Contango is basically the opposite situation of normal backwardation.

It occurs when the current futures price of a commodity or other financial instrument trades above the current spot price of the underlying instrument, which indicates that the futures price shall eventually fall to converge with the spot price.

Similar to backwardation, a futures contract that is in contango will gradually approach the spot price over time as the contract approaches its expiration date.

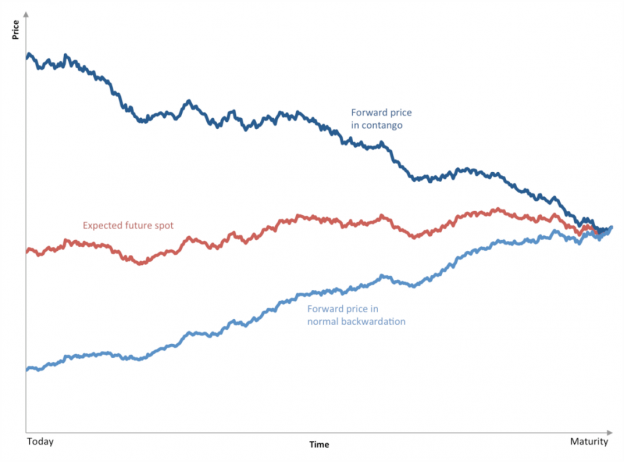

The following chart shows how a contango and backwardation curve looks like as the futures contract approaches its maturity.

A futures price that is in contango will fall over time, while a futures price that is in backwardation will rise over time, given the expected spot price remains more or less stable, i.e. above the futures price in backwardation, and below the futures price in contango.

As can be seen on the chart, prices in contango are down sloping, while the opposite is true for prices in backwardation.

This can be easily observed by following forward curves of any financial instrument.